Artificial Intelligence In Military Market Size, Share | Report 2023-2032

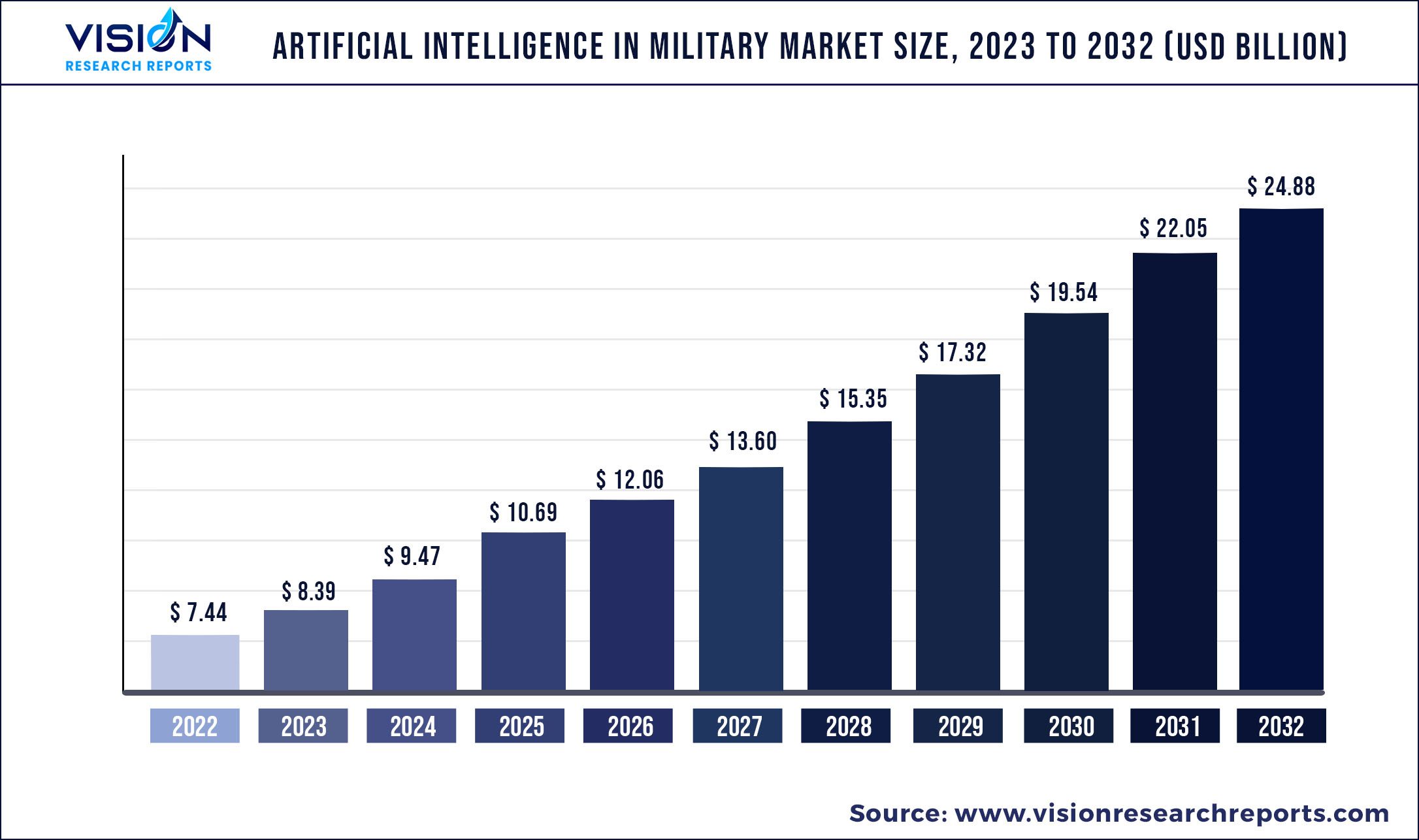

The global artificial intelligence in military market size was estimated at around USD 7.44 billion in 2022 and it is projected to hit around USD 24.88 billion by 2032, growing at a CAGR of 12.83% from 2023 to 2032.

Key Pointers

| Report Coverage | Details |

| Market Size in 2022 | USD 7.44 billion |

| Revenue Forecast by 2032 | USD 24.88 billion |

| Growth rate from 2023 to 2032 | CAGR of 12.83% |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Companies Covered | Lockheed Martin Corporation; BAE Systems, Inc.; Northrop Grumman Corporation; Raytheon Technologies;Rafael Advanced Defense Systems; SparkCognition; L3Harris Technologies Inc.;International Business Machines Corporation; Thales Group |

Increased government spending on the R&D of military weaponry with AI capabilities, development of specialized AI chips, growing adoption of big data in the defense industry, growing private investment in the R&D of AI-based military technology, and incidence of animosity and cross-border wars in various countries are some of the main factors anticipated to propel the growth of AI in the military sector. For instance, in June 2022, The Ministry of Defense (MoD) announced the U.K.'s Defense AI Strategy, which stated the safe, ambitious, and responsible use of AI and a set of ethical guidelines designed to govern the military and defense sectors' use of AI.

Training and simulation are broad fields combining system and software engineering principles to build models that can help soldiers train on various fighting systems used in military operations.U.S. Army is investing significant time and resources in virtual reality (VR), augmented reality (AR), and mixed reality (MR) equipment and training to make infantry safer and better prepared. For instance, in October 2022, as part of an operational assessment coordinated by the U.S. Army Test and Evaluation Command, Fort Hood's Combat Tactical Training Center hosted 150 soldiers to prepare them for realistic battlefield training.

The rising use of AI-powered cybersecurity is anticipated to increase the need for artificial intelligence in the military sector during the projected period. In October 2022, the Georgia Institute of Technology granted a $22.7 million contract by the U.S. Defense Advanced Research Projects Agency (DARP) to create strategies for identifying, controlling, and defeating hackers and assisting in the integration of cybersecurity. AI chips have increased, with chipmakers developing various types of these chips to power AI applications like computer vision, natural language processing, network security, and robotics across a wide range of industries, including automotive, IT, retail, and healthcare.

Regional Insights

North America registered the largest revenue share of 35.3% in 2022, due to the increasing investment in artificial intelligence technologies by the major countries in North America. The U.S. dominates this sector and is investing in AI. systems to preserve its military dominance and reduce the risk of possible network threats.

For instance, In November 2020, C3.ai, Inc., an enterprise A.I. software provider, announced a collaboration with Raytheon Intelligence & Space, a producer of advanced sensors, training, software, and hardware. This collaboration aimed to create artificial intelligence programs for aerospace and defense operations for government clients, such as the U.S. Air Force and the intelligence community.

Market revenue in Europe is anticipated to grow significantly throughout the forecast period due to Russia's modernization of its weapons. The Russian government invested considerable money in creating information management technologies to improve decision-making in actual combat circumstances.

For instance, in August 2022, The Russian Ministry of Defense introduced a department dedicated to developing artificial intelligence weapons. A new department is created to accelerate work on the application of artificial intelligence technology to produce models of firearms for military and special equipment.

Artificial Intelligence In Military Market Segmentations:

| By Offering | By Application | By Technology | By Platform | By Installation |

|

Hardware Software Services |

Warfare Platform Cyber Security Logistics & Transportation Surveillance & Situational Awareness Command & Control Battlefield Healthcare Simulation & Training Information Processing Threat Detection Others |

Machine Learning Deep Learning Natural Language Processing Context-Aware Computing Computer Vision Intelligent Virtual Agent (Iva) /Virtual Agents Others |

Land Naval Airborne Space |

New Procurement Upgradation |

Chapter 1. Introduction

1.1. Research Objective

1.2. Scope of the Study

1.3. Definition

Chapter 2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.3. Assumptions & Limitations

Chapter 3. Executive Summary

3.1. Market Snapshot

Chapter 4. Market Variables and Scope

4.1. Introduction

4.2. Market Classification and Scope

4.3. Industry Value Chain Analysis

4.3.1. Raw Material Procurement Analysis

4.3.2. Sales and Distribution Channel Analysis

4.3.3. Downstream Buyer Analysis

Chapter 5. COVID 19 Impact on Artificial Intelligence In Military Market

5.1. COVID-19 Landscape: Artificial Intelligence In Military Industry Impact

5.2. COVID 19 - Impact Assessment for the Industry

5.3. COVID 19 Impact: Global Major Government Policy

5.4. Market Trends and Opportunities in the COVID-19 Landscape

Chapter 6. Market Dynamics Analysis and Trends

6.1. Market Dynamics

6.1.1. Market Drivers

6.1.2. Market Restraints

6.1.3. Market Opportunities

6.2. Porter’s Five Forces Analysis

6.2.1. Bargaining power of suppliers

6.2.2. Bargaining power of buyers

6.2.3. Threat of substitute

6.2.4. Threat of new entrants

6.2.5. Degree of competition

Chapter 7. Competitive Landscape

7.1.1. Company Market Share/Positioning Analysis

7.1.2. Key Strategies Adopted by Players

7.1.3. Vendor Landscape

7.1.3.1. List of Suppliers

7.1.3.2. List of Buyers

Chapter 8. Global Artificial Intelligence In Military Market, By Offering

8.1. Artificial Intelligence In Military Market, by Offering, 2023-2032

8.1.1. Hardware

8.1.1.1. Market Revenue and Forecast (2020-2032)

8.1.2. Software

8.1.2.1. Market Revenue and Forecast (2020-2032)

8.1.3. Services

8.1.3.1. Market Revenue and Forecast (2020-2032)

Chapter 9. Global Artificial Intelligence In Military Market, By Application

9.1. Artificial Intelligence In Military Market, by Application, 2023-2032

9.1.1. Warfare Platform

9.1.1.1. Market Revenue and Forecast (2020-2032)

9.1.2. Cyber Security

9.1.2.1. Market Revenue and Forecast (2020-2032)

9.1.3. Logistics & Transportation

9.1.3.1. Market Revenue and Forecast (2020-2032)

9.1.4. Surveillance & Situational Awareness

9.1.4.1. Market Revenue and Forecast (2020-2032)

9.1.5. Command & Control

9.1.5.1. Market Revenue and Forecast (2020-2032)

9.1.6. Battlefield Healthcare

9.1.6.1. Market Revenue and Forecast (2020-2032)

9.1.7. Simulation & Training

9.1.7.1. Market Revenue and Forecast (2020-2032)

9.1.8. Information Processing

9.1.8.1. Market Revenue and Forecast (2020-2032)

9.1.9. Threat Detection

9.1.9.1. Market Revenue and Forecast (2020-2032)

9.1.10. Others

9.1.10.1. Market Revenue and Forecast (2020-2032)

Chapter 10. Global Artificial Intelligence In Military Market, By Technology

10.1. Artificial Intelligence In Military Market, by Technology, 2023-2032

10.1.1. Machine Learning

10.1.1.1. Market Revenue and Forecast (2020-2032)

10.1.2. Deep Learning

10.1.2.1. Market Revenue and Forecast (2020-2032)

10.1.3. Natural Language Processing

10.1.3.1. Market Revenue and Forecast (2020-2032)

10.1.4. Context-Aware Computing

10.1.4.1. Market Revenue and Forecast (2020-2032)

10.1.5. Computer Vision

10.1.5.1. Market Revenue and Forecast (2020-2032)

10.1.6. Intelligent Virtual Agent (Iva) /Virtual Agents

10.1.6.1. Market Revenue and Forecast (2020-2032)

10.1.7. Others

10.1.7.1. Market Revenue and Forecast (2020-2032)

Chapter 11. Global Artificial Intelligence In Military Market, By Platform

11.1. Artificial Intelligence In Military Market, by Platform, 2023-2032

11.1.1. Land

11.1.1.1. Market Revenue and Forecast (2020-2032)

11.1.2. Naval

11.1.2.1. Market Revenue and Forecast (2020-2032)

11.1.3. Airborne

11.1.3.1. Market Revenue and Forecast (2020-2032)

11.1.4. Space

11.1.4.1. Market Revenue and Forecast (2020-2032)

Chapter 12. Global Artificial Intelligence In Military Market, By Installation

12.1. Artificial Intelligence In Military Market, by Installation, 2023-2032

12.1.1. New Procurement

12.1.1.1. Market Revenue and Forecast (2020-2032)

12.1.2. Upgradation

12.1.2.1. Market Revenue and Forecast (2020-2032)

Chapter 13. Global Artificial Intelligence In Military Market, Regional Estimates and Trend Forecast

13.1. North America

13.1.1. Market Revenue and Forecast, by Offering (2020-2032)

13.1.2. Market Revenue and Forecast, by Application (2020-2032)

13.1.3. Market Revenue and Forecast, by Technology (2020-2032)

13.1.4. Market Revenue and Forecast, by Platform (2020-2032)

13.1.5. Market Revenue and Forecast, by Installation (2020-2032)

13.1.6. U.S.

13.1.6.1. Market Revenue and Forecast, by Offering (2020-2032)

13.1.6.2. Market Revenue and Forecast, by Application (2020-2032)

13.1.6.3. Market Revenue and Forecast, by Technology (2020-2032)

13.1.6.4. Market Revenue and Forecast, by Platform (2020-2032)

13.1.7. Market Revenue and Forecast, by Installation (2020-2032)

13.1.8. Rest of North America

13.1.8.1. Market Revenue and Forecast, by Offering (2020-2032)

13.1.8.2. Market Revenue and Forecast, by Application (2020-2032)

13.1.8.3. Market Revenue and Forecast, by Technology (2020-2032)

13.1.8.4. Market Revenue and Forecast, by Platform (2020-2032)

13.1.8.5. Market Revenue and Forecast, by Installation (2020-2032)

13.2. Europe

13.2.1. Market Revenue and Forecast, by Offering (2020-2032)

13.2.2. Market Revenue and Forecast, by Application (2020-2032)

13.2.3. Market Revenue and Forecast, by Technology (2020-2032)

13.2.4. Market Revenue and Forecast, by Platform (2020-2032)

13.2.5. Market Revenue and Forecast, by Installation (2020-2032)

13.2.6. UK

13.2.6.1. Market Revenue and Forecast, by Offering (2020-2032)

13.2.6.2. Market Revenue and Forecast, by Application (2020-2032)

13.2.6.3. Market Revenue and Forecast, by Technology (2020-2032)

13.2.7. Market Revenue and Forecast, by Platform (2020-2032)

13.2.8. Market Revenue and Forecast, by Installation (2020-2032)

13.2.9. Germany

13.2.9.1. Market Revenue and Forecast, by Offering (2020-2032)

13.2.9.2. Market Revenue and Forecast, by Application (2020-2032)

13.2.9.3. Market Revenue and Forecast, by Technology (2020-2032)

13.2.10. Market Revenue and Forecast, by Platform (2020-2032)

13.2.11. Market Revenue and Forecast, by Installation (2020-2032)

13.2.12. France

13.2.12.1. Market Revenue and Forecast, by Offering (2020-2032)

13.2.12.2. Market Revenue and Forecast, by Application (2020-2032)

13.2.12.3. Market Revenue and Forecast, by Technology (2020-2032)

13.2.12.4. Market Revenue and Forecast, by Platform (2020-2032)

13.2.13. Market Revenue and Forecast, by Installation (2020-2032)

13.2.14. Rest of Europe

13.2.14.1. Market Revenue and Forecast, by Offering (2020-2032)

13.2.14.2. Market Revenue and Forecast, by Application (2020-2032)

13.2.14.3. Market Revenue and Forecast, by Technology (2020-2032)

13.2.14.4. Market Revenue and Forecast, by Platform (2020-2032)

13.2.15. Market Revenue and Forecast, by Installation (2020-2032)

13.3. APAC

13.3.1. Market Revenue and Forecast, by Offering (2020-2032)

13.3.2. Market Revenue and Forecast, by Application (2020-2032)

13.3.3. Market Revenue and Forecast, by Technology (2020-2032)

13.3.4. Market Revenue and Forecast, by Platform (2020-2032)

13.3.5. Market Revenue and Forecast, by Installation (2020-2032)

13.3.6. India

13.3.6.1. Market Revenue and Forecast, by Offering (2020-2032)

13.3.6.2. Market Revenue and Forecast, by Application (2020-2032)

13.3.6.3. Market Revenue and Forecast, by Technology (2020-2032)

13.3.6.4. Market Revenue and Forecast, by Platform (2020-2032)

13.3.7. Market Revenue and Forecast, by Installation (2020-2032)

13.3.8. China

13.3.8.1. Market Revenue and Forecast, by Offering (2020-2032)

13.3.8.2. Market Revenue and Forecast, by Application (2020-2032)

13.3.8.3. Market Revenue and Forecast, by Technology (2020-2032)

13.3.8.4. Market Revenue and Forecast, by Platform (2020-2032)

13.3.9. Market Revenue and Forecast, by Installation (2020-2032)

13.3.10. Japan

13.3.10.1. Market Revenue and Forecast, by Offering (2020-2032)

13.3.10.2. Market Revenue and Forecast, by Application (2020-2032)

13.3.10.3. Market Revenue and Forecast, by Technology (2020-2032)

13.3.10.4. Market Revenue and Forecast, by Platform (2020-2032)

13.3.10.5. Market Revenue and Forecast, by Installation (2020-2032)

13.3.11. Rest of APAC

13.3.11.1. Market Revenue and Forecast, by Offering (2020-2032)

13.3.11.2. Market Revenue and Forecast, by Application (2020-2032)

13.3.11.3. Market Revenue and Forecast, by Technology (2020-2032)

13.3.11.4. Market Revenue and Forecast, by Platform (2020-2032)

13.3.11.5. Market Revenue and Forecast, by Installation (2020-2032)

13.4. MEA

13.4.1. Market Revenue and Forecast, by Offering (2020-2032)

13.4.2. Market Revenue and Forecast, by Application (2020-2032)

13.4.3. Market Revenue and Forecast, by Technology (2020-2032)

13.4.4. Market Revenue and Forecast, by Platform (2020-2032)

13.4.5. Market Revenue and Forecast, by Installation (2020-2032)

13.4.6. GCC

13.4.6.1. Market Revenue and Forecast, by Offering (2020-2032)

13.4.6.2. Market Revenue and Forecast, by Application (2020-2032)

13.4.6.3. Market Revenue and Forecast, by Technology (2020-2032)

13.4.6.4. Market Revenue and Forecast, by Platform (2020-2032)

13.4.7. Market Revenue and Forecast, by Installation (2020-2032)

13.4.8. North Africa

13.4.8.1. Market Revenue and Forecast, by Offering (2020-2032)

13.4.8.2. Market Revenue and Forecast, by Application (2020-2032)

13.4.8.3. Market Revenue and Forecast, by Technology (2020-2032)

13.4.8.4. Market Revenue and Forecast, by Platform (2020-2032)

13.4.9. Market Revenue and Forecast, by Installation (2020-2032)

13.4.10. South Africa

13.4.10.1. Market Revenue and Forecast, by Offering (2020-2032)

13.4.10.2. Market Revenue and Forecast, by Application (2020-2032)

13.4.10.3. Market Revenue and Forecast, by Technology (2020-2032)

13.4.10.4. Market Revenue and Forecast, by Platform (2020-2032)

13.4.10.5. Market Revenue and Forecast, by Installation (2020-2032)

13.4.11. Rest of MEA

13.4.11.1. Market Revenue and Forecast, by Offering (2020-2032)

13.4.11.2. Market Revenue and Forecast, by Application (2020-2032)

13.4.11.3. Market Revenue and Forecast, by Technology (2020-2032)

13.4.11.4. Market Revenue and Forecast, by Platform (2020-2032)

13.4.11.5. Market Revenue and Forecast, by Installation (2020-2032)

13.5. Latin America

13.5.1. Market Revenue and Forecast, by Offering (2020-2032)

13.5.2. Market Revenue and Forecast, by Application (2020-2032)

13.5.3. Market Revenue and Forecast, by Technology (2020-2032)

13.5.4. Market Revenue and Forecast, by Platform (2020-2032)

13.5.5. Market Revenue and Forecast, by Installation (2020-2032)

13.5.6. Brazil

13.5.6.1. Market Revenue and Forecast, by Offering (2020-2032)

13.5.6.2. Market Revenue and Forecast, by Application (2020-2032)

13.5.6.3. Market Revenue and Forecast, by Technology (2020-2032)

13.5.6.4. Market Revenue and Forecast, by Platform (2020-2032)

13.5.7. Market Revenue and Forecast, by Installation (2020-2032)

13.5.8. Rest of LATAM

13.5.8.1. Market Revenue and Forecast, by Offering (2020-2032)

13.5.8.2. Market Revenue and Forecast, by Application (2020-2032)

13.5.8.3. Market Revenue and Forecast, by Technology (2020-2032)

13.5.8.4. Market Revenue and Forecast, by Platform (2020-2032)

13.5.8.5. Market Revenue and Forecast, by Installation (2020-2032)

Chapter 14. Company Profiles

14.1. Lockheed Martin Corporation

14.1.1. Company Overview

14.1.2. Product Offerings

14.1.3. Financial Performance

14.1.4. Recent Initiatives

14.2. BAE Systems, Inc.

14.2.1. Company Overview

14.2.2. Product Offerings

14.2.3. Financial Performance

14.2.4. Recent Initiatives

14.3. Northrop Grumman Corporation

14.3.1. Company Overview

14.3.2. Product Offerings

14.3.3. Financial Performance

14.3.4. Recent Initiatives

14.4. Raytheon Technologies

14.4.1. Company Overview

14.4.2. Product Offerings

14.4.3. Financial Performance

14.4.4. Recent Initiatives

14.5. Rafael Advanced Defense Systems

14.5.1. Company Overview

14.5.2. Product Offerings

14.5.3. Financial Performance

14.5.4. Recent Initiatives

14.6. Rafael Advanced Defense Systems

14.6.1. Company Overview

14.6.2. Product Offerings

14.6.3. Financial Performance

14.6.4. Recent Initiatives

14.7. L3Harris Technologies Inc.

14.7.1. Company Overview

14.7.2. Product Offerings

14.7.3. Financial Performance

14.7.4. Recent Initiatives

14.8. International Business Machines Corporation

14.8.1. Company Overview

14.8.2. Product Offerings

14.8.3. Financial Performance

14.8.4. Recent Initiatives

14.9. Thales Group

14.9.1. Company Overview

14.9.2. Product Offerings

14.9.3. Financial Performance

14.9.4. Recent Initiatives

Chapter 15. Research Methodology

15.1. Primary Research

15.2. Secondary Research

15.3. Assumptions

Chapter 16. Appendix

16.1. About Us

16.2. Glossary of Terms

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers