Intraoperative Imaging Market Size, Trends, Share, Growth | Report 2023-2032

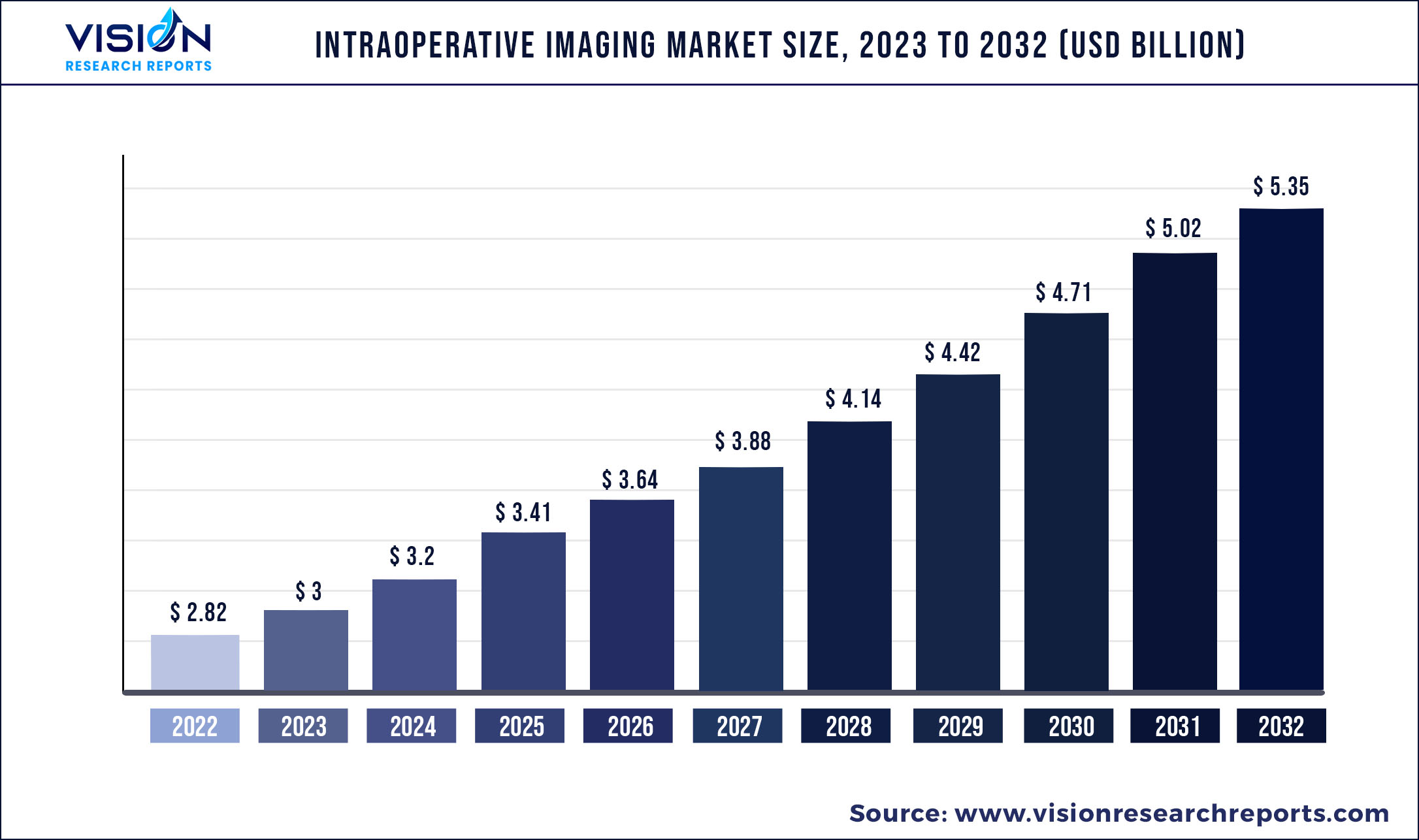

The global intraoperative imaging market was valued at USD 2.82 billion in 2022 and it is predicted to surpass around USD 5.35 billion by 2032 with a CAGR of 6.64% from 2023 to 2032.

Key Pointers

Report Scope of the Intraoperative Imaging Market

| Report Coverage | Details |

| Market Size in 2022 | USD 2.82 billion |

| Revenue Forecast by 2032 | USD 5.35 billion |

| Growth rate from 2023 to 2032 | CAGR of 6.64% |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Market Analysis (Terms Used) | Value (US$ Million/Billion) or (Volume/Units) |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

The market growth can be attributed to the increase in the adoption of minimally invasive surgeries coupled with technological advancements. In addition, the increasing prevalence of chronic disorders and the rise in the geriatric population are major factors contributing to the market growth. The global geriatric population has grown dramatically, putting them at risk for various disorders. As per the UN, in 2017, the global population of people aged 60 and above was 962 million, doubling in 2050 to reach over 2.1 billion.

Intraoperative imaging is getting popular as a critical tool for more precise and effective surgeries, which improves patient outcomes while also enhancing workflows and efficiencies for healthcare personnel in and out of the operating room.

Intraoperative imaging technologies, such as iUltrasound, C-arm, and iMRI, have greatly extended surgical possibilities. The ability to see bones and soft tissue with extreme precision has transformed the surgical care of a variety of disorders, including neurology, orthopedics, cardiology, vascular, and neurology. The constant advances in intraoperative imaging technologies, such as 3D technology and real-time imaging, are expected to boost market expansion. For instance, in March 2021, the FDA granted GE Healthcare clearance for OEC 3D, a surgical imaging system capable of both 3D and 2D imaging. By providing precise volumetric images, OEC 3D aims to set a benchmark for intraoperative 3D imaging for spine and orthopedic surgeries.

An increase in the adoption of minimally invasive surgeries, which is highly dependent on the imaging chain, as the medical team has to rely on indirect visualization of the surgical field during the entire procedure, is expected to promote market growth. However, constraints such as the high cost of intraoperative imaging systems and an increase in demand for refurbished imaging systems may hinder the market expansion throughout the projected period.

The COVID-19 pandemic has significantly affected the intraoperative imaging market. Delay in surgical procedures is the reason. The medical settings where these imaging systems are used are high-risk areas for the spread of the COVID-19 infection. However, guidelines for safe and effective surgical care will decrease pandemic implications during the forecast period. Furthermore, raw material shortages are causing broad business interruptions, resulting in a decline in imaging equipment manufacturing and transportation disruptions. On the other hand, now that the lockdown limitations have been lifted, the market is gradually getting back to normal.

Competitive Insights

The key players are working to improve their product offerings by upgrading their products, leveraging important cooperative drives, as well as considering acquisitions and government approvals to increase their client base and get a larger part of the entire industry. For instance, in September 2021, GE Healthcare agreed to acquire BK Medical, a leader in advanced surgical visualization. With this agreement, BK Medical's active imaging platform will be able to reach new customers and markets around the world. In addition, the combination of GE Healthcare's diagnostic imaging technology and BK's ability to enable decision-making and surgical visualization in the intervention will allow for better decision-making across the healthcare system. The following are some of the major participants in the global intraoperative imaging market:

Intraoperative Imaging Market Segmentations:

| By Product | By Component | By Application | By End-use |

|

iCT iUltrasound iMRI C-arm system |

System Software Services |

Neurosurgery Orthopedic ENT surgery Oncology surgery Trauma surgery/ emergency room Cardiovascular Others |

Hospital Others |

Chapter 1. Introduction

1.1. Research Objective

1.2. Scope of the Study

1.3. Definition

Chapter 2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.3. Assumptions & Limitations

Chapter 3. Executive Summary

3.1. Market Snapshot

Chapter 4. Market Variables and Scope

4.1. Introduction

4.2. Market Classification and Scope

4.3. Industry Value Chain Analysis

4.3.1. Raw Material Procurement Analysis

4.3.2. Sales and Distribution Channel Analysis

4.3.3. Downstream Buyer Analysis

Chapter 5. COVID 19 Impact on Intraoperative Imaging Market

5.1. COVID-19 Landscape: Intraoperative Imaging Industry Impact

5.2. COVID 19 - Impact Assessment for the Industry

5.3. COVID 19 Impact: Global Major Government Policy

5.4. Market Trends and Opportunities in the COVID-19 Landscape

Chapter 6. Market Dynamics Analysis and Trends

6.1. Market Dynamics

6.1.1. Market Drivers

6.1.2. Market Restraints

6.1.3. Market Opportunities

6.2. Porter’s Five Forces Analysis

6.2.1. Bargaining power of suppliers

6.2.2. Bargaining power of buyers

6.2.3. Threat of substitute

6.2.4. Threat of new entrants

6.2.5. Degree of competition

Chapter 7. Competitive Landscape

7.1.1. Company Market Share/Positioning Analysis

7.1.2. Key Strategies Adopted by Players

7.1.3. Vendor Landscape

7.1.3.1. List of Suppliers

7.1.3.2. List of Buyers

Chapter 8. Global Intraoperative Imaging Market, By Product

8.1. Intraoperative Imaging Market, by Product, 2023-2032

8.1.1. iCT

8.1.1.1. Market Revenue and Forecast (2020-2032)

8.1.2. iUltrasound

8.1.2.1. Market Revenue and Forecast (2020-2032)

8.1.3. iMRI

8.1.3.1. Market Revenue and Forecast (2020-2032)

8.1.4. C-arm system

8.1.4.1. Market Revenue and Forecast (2020-2032)

Chapter 9. Global Intraoperative Imaging Market, By Component

9.1. Intraoperative Imaging Market, by Component, 2023-2032

9.1.1. System

9.1.1.1. Market Revenue and Forecast (2020-2032)

9.1.2. Software

9.1.2.1. Market Revenue and Forecast (2020-2032)

9.1.3. Services

9.1.3.1. Market Revenue and Forecast (2020-2032)

Chapter 10. Global Intraoperative Imaging Market, By Application

10.1. Intraoperative Imaging Market, by Application, 2023-2032

10.1.1. Neurosurgery

10.1.1.1. Market Revenue and Forecast (2020-2032)

10.1.2. Orthopedic

10.1.2.1. Market Revenue and Forecast (2020-2032)

10.1.3. ENT surgery

10.1.3.1. Market Revenue and Forecast (2020-2032)

10.1.4. Oncology surgery

10.1.4.1. Market Revenue and Forecast (2020-2032)

10.1.5. Trauma surgery/ emergency room

10.1.5.1. Market Revenue and Forecast (2020-2032)

10.1.6. Cardiovascular

10.1.6.1. Market Revenue and Forecast (2020-2032)

10.1.7. Others

10.1.7.1. Market Revenue and Forecast (2020-2032)

Chapter 11. Global Intraoperative Imaging Market, By End-use

11.1. Intraoperative Imaging Market, by End-use, 2023-2032

11.1.1. Hospital

11.1.1.1. Market Revenue and Forecast (2020-2032)

11.1.2. Others

11.1.2.1. Market Revenue and Forecast (2020-2032)

Chapter 12. Global Intraoperative Imaging Market, Regional Estimates and Trend Forecast

12.1. North America

12.1.1. Market Revenue and Forecast, by Product (2020-2032)

12.1.2. Market Revenue and Forecast, by Component (2020-2032)

12.1.3. Market Revenue and Forecast, by Application (2020-2032)

12.1.4. Market Revenue and Forecast, by End-use (2020-2032)

12.1.5. U.S.

12.1.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.1.5.2. Market Revenue and Forecast, by Component (2020-2032)

12.1.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.1.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.1.6. Rest of North America

12.1.6.1. Market Revenue and Forecast, by Product (2020-2032)

12.1.6.2. Market Revenue and Forecast, by Component (2020-2032)

12.1.6.3. Market Revenue and Forecast, by Application (2020-2032)

12.1.6.4. Market Revenue and Forecast, by End-use (2020-2032)

12.2. Europe

12.2.1. Market Revenue and Forecast, by Product (2020-2032)

12.2.2. Market Revenue and Forecast, by Component (2020-2032)

12.2.3. Market Revenue and Forecast, by Application (2020-2032)

12.2.4. Market Revenue and Forecast, by End-use (2020-2032)

12.2.5. UK

12.2.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.2.5.2. Market Revenue and Forecast, by Component (2020-2032)

12.2.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.2.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.2.6. Germany

12.2.6.1. Market Revenue and Forecast, by Product (2020-2032)

12.2.6.2. Market Revenue and Forecast, by Component (2020-2032)

12.2.6.3. Market Revenue and Forecast, by Application (2020-2032)

12.2.6.4. Market Revenue and Forecast, by End-use (2020-2032)

12.2.7. France

12.2.7.1. Market Revenue and Forecast, by Product (2020-2032)

12.2.7.2. Market Revenue and Forecast, by Component (2020-2032)

12.2.7.3. Market Revenue and Forecast, by Application (2020-2032)

12.2.7.4. Market Revenue and Forecast, by End-use (2020-2032)

12.2.8. Rest of Europe

12.2.8.1. Market Revenue and Forecast, by Product (2020-2032)

12.2.8.2. Market Revenue and Forecast, by Component (2020-2032)

12.2.8.3. Market Revenue and Forecast, by Application (2020-2032)

12.2.8.4. Market Revenue and Forecast, by End-use (2020-2032)

12.3. APAC

12.3.1. Market Revenue and Forecast, by Product (2020-2032)

12.3.2. Market Revenue and Forecast, by Component (2020-2032)

12.3.3. Market Revenue and Forecast, by Application (2020-2032)

12.3.4. Market Revenue and Forecast, by End-use (2020-2032)

12.3.5. India

12.3.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.3.5.2. Market Revenue and Forecast, by Component (2020-2032)

12.3.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.3.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.3.6. China

12.3.6.1. Market Revenue and Forecast, by Product (2020-2032)

12.3.6.2. Market Revenue and Forecast, by Component (2020-2032)

12.3.6.3. Market Revenue and Forecast, by Application (2020-2032)

12.3.6.4. Market Revenue and Forecast, by End-use (2020-2032)

12.3.7. Japan

12.3.7.1. Market Revenue and Forecast, by Product (2020-2032)

12.3.7.2. Market Revenue and Forecast, by Component (2020-2032)

12.3.7.3. Market Revenue and Forecast, by Application (2020-2032)

12.3.7.4. Market Revenue and Forecast, by End-use (2020-2032)

12.3.8. Rest of APAC

12.3.8.1. Market Revenue and Forecast, by Product (2020-2032)

12.3.8.2. Market Revenue and Forecast, by Component (2020-2032)

12.3.8.3. Market Revenue and Forecast, by Application (2020-2032)

12.3.8.4. Market Revenue and Forecast, by End-use (2020-2032)

12.4. MEA

12.4.1. Market Revenue and Forecast, by Product (2020-2032)

12.4.2. Market Revenue and Forecast, by Component (2020-2032)

12.4.3. Market Revenue and Forecast, by Application (2020-2032)

12.4.4. Market Revenue and Forecast, by End-use (2020-2032)

12.4.5. GCC

12.4.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.4.5.2. Market Revenue and Forecast, by Component (2020-2032)

12.4.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.4.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.4.6. North Africa

12.4.6.1. Market Revenue and Forecast, by Product (2020-2032)

12.4.6.2. Market Revenue and Forecast, by Component (2020-2032)

12.4.6.3. Market Revenue and Forecast, by Application (2020-2032)

12.4.6.4. Market Revenue and Forecast, by End-use (2020-2032)

12.4.7. South Africa

12.4.7.1. Market Revenue and Forecast, by Product (2020-2032)

12.4.7.2. Market Revenue and Forecast, by Component (2020-2032)

12.4.7.3. Market Revenue and Forecast, by Application (2020-2032)

12.4.7.4. Market Revenue and Forecast, by End-use (2020-2032)

12.4.8. Rest of MEA

12.4.8.1. Market Revenue and Forecast, by Product (2020-2032)

12.4.8.2. Market Revenue and Forecast, by Component (2020-2032)

12.4.8.3. Market Revenue and Forecast, by Application (2020-2032)

12.4.8.4. Market Revenue and Forecast, by End-use (2020-2032)

12.5. Latin America

12.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.5.2. Market Revenue and Forecast, by Component (2020-2032)

12.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.5.5. Brazil

12.5.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.5.5.2. Market Revenue and Forecast, by Component (2020-2032)

12.5.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.5.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.5.6. Rest of LATAM

12.5.6.1. Market Revenue and Forecast, by Product (2020-2032)

12.5.6.2. Market Revenue and Forecast, by Component (2020-2032)

12.5.6.3. Market Revenue and Forecast, by Application (2020-2032)

12.5.6.4. Market Revenue and Forecast, by End-use (2020-2032)

Chapter 13. Company Profiles

13.1. GE Healthcare

13.1.1. Company Overview

13.1.2. Product Offerings

13.1.3. Financial Performance

13.1.4. Recent Initiatives

13.2. Siemens Healthineers AG

13.2.1. Company Overview

13.2.2. Product Offerings

13.2.3. Financial Performance

13.2.4. Recent Initiatives

13.3. Koninklijke Philips N.V.

13.3.1. Company Overview

13.3.2. Product Offerings

13.3.3. Financial Performance

13.3.4. Recent Initiatives

13.4. Medtronic

13.4.1. Company Overview

13.4.2. Product Offerings

13.4.3. Financial Performance

13.4.4. Recent Initiatives

13.5. Ziehm Imaging GmbH

13.5.1. Company Overview

13.5.2. Product Offerings

13.5.3. Financial Performance

13.5.4. Recent Initiatives

13.6. IMRIS

13.6.1. Company Overview

13.6.2. Product Offerings

13.6.3. Financial Performance

13.6.4. Recent Initiatives

13.7. Shimadzu Corporation

13.7.1. Company Overview

13.7.2. Product Offerings

13.7.3. Financial Performance

13.7.4. Recent Initiatives

13.8. NeuroLogica

13.8.1. Company Overview

13.8.2. Product Offerings

13.8.3. Financial Performance

13.8.4. Recent Initiatives

Chapter 14. Research Methodology

14.1. Primary Research

14.2. Secondary Research

14.3. Assumptions

Chapter 15. Appendix

15.1. About Us

15.2. Glossary of Terms

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers