Vessel Sealing Devices Market Size, Share, Growth, Trends, Revenue 2023-2032

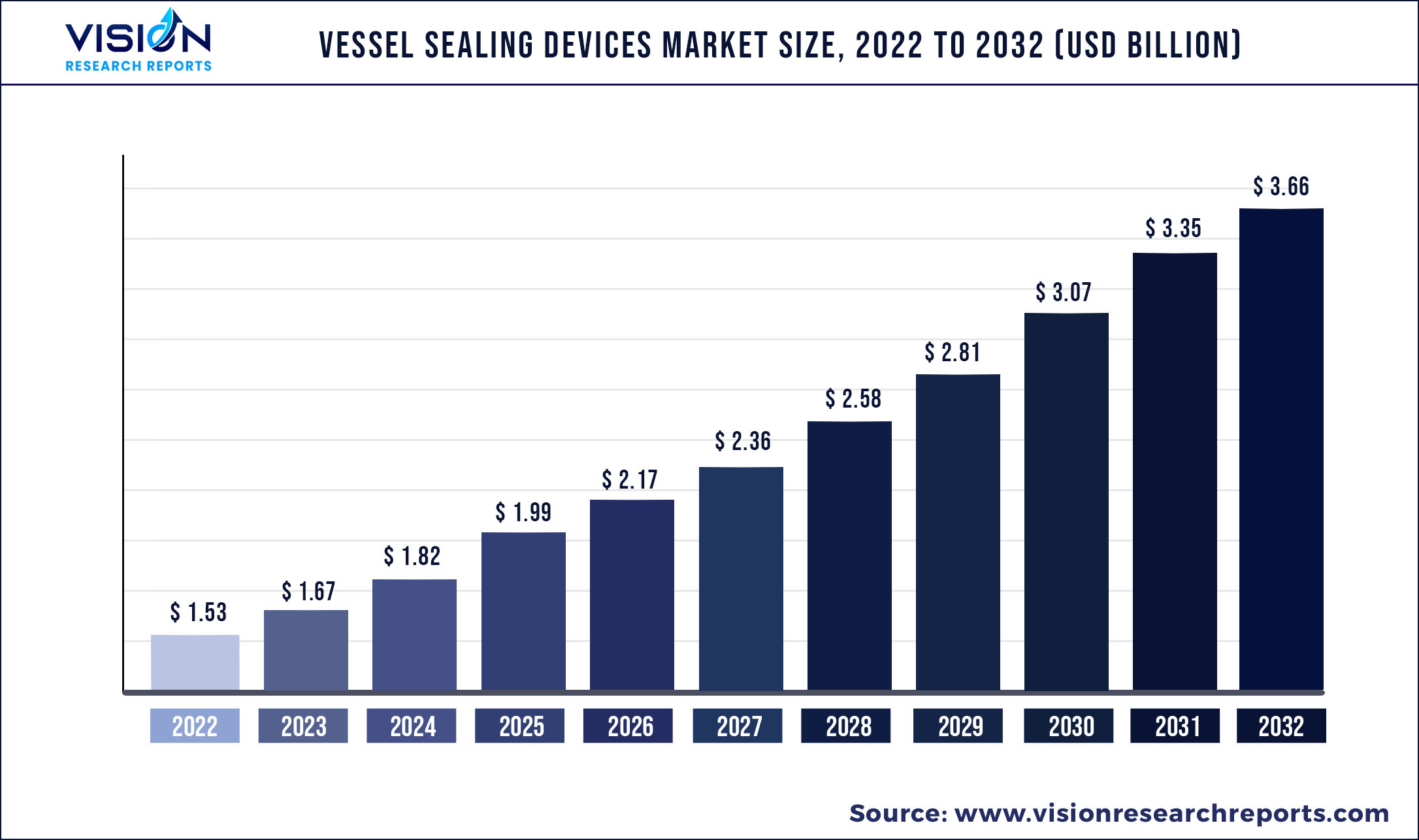

The global vessel sealing devices market was valued at USD 1.53 billion in 2022 and it is predicted to surpass around USD 3.66 billion by 2032 with a CAGR of 9.1% from 2023 to 2032.

Key Pointers

| Report Coverage | Details |

| Market Size in 2022 | USD 1.53 billion |

| Revenue Forecast by 2032 | USD 3.66 billion |

| Growth rate from 2023 to 2032 | CAGR of 9.1% |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Companies Covered | Medtronic; Olympus Corporation; B. Braun Melsungen AG; Medical Devices Business Services, Inc. (Johnson & Johnson); Erbe Elektromedizin GmbH; Bowa Medical; OmniGuide Holdings, Inc.; Intuitive Surgical; Bolder Surgical LLC; KLS Martin Group |

Growing product developments, surgical procedures, and preference for minimally invasive surgeries are some of the key drivers of this market. Medtronic, a market leader in vessel sealing devices, for example, registered record sales of USD 5.4 million in its surgical innovations portfolio comprising advanced energy, stapling, and visualization devices. This was owing to a strong portfolio with continuous product enhancements.

One of the main drivers boosting the market is the rising geriatric population, which is more prone to chronic ailments. Axillary dissection, chronic hepatitis, colorectal cancer, and other conditions are among the many conditions that are often treated with vessel sealing devices. Additionally, the broad use of the product in laparoscopic procedures, which are less invasive and result in less postoperative pain, is boosting market expansion. In addition, the development of bipolar devices, which help in stronger and more uniform compression, and ultrasound technology, which monitors the distribution of heat and energy, are giving the industry a boost.

Additionally, the growing need for safe and efficient surgical instruments to lower infection rates and blood loss is driving up overall sales of vessel sealing devices, which is benefiting the market's expansion. The market is predicted to grow as a result of a number of additional variables, such as the development of cutting-edge, high-quality vessel sealing devices, an increase in gynecological, urological, cardiovascular, and orthopedic operations, and a sizable expansion of the medical sector.

Rising product improvement is a key driver contributing to the growth of the market for vessel sealing devices. This is due to the growing demand for vessel sealing devices that offer better consistency, utility, reliability, efficiency, and safety. According to an article published in the International Journal of Scientific Research, an ideal vessel sealing device is effective on vessels having a diameter less than or equal to 7mm, produces minimal thermal spread, works quickly, is reusable, and produces consistent results. Market players are also involved in integrating these devices into robotic surgical systems. For example, Intuitive Surgical’s SynchroSeal is compatible with the da Vinci surgical system and enables the user to quickly seal and cut vessels up to 5 mm in diameter.

Vessel Sealing Devices Market Segmentations:

| By Application | By Product | By End-use |

|

General Surgery Laparoscopic Surgery |

Generators Instruments Accessories |

Hospitals & Specialty Clinics Ambulatory Surgical Centers |

Chapter 1. Introduction

1.1. Research Objective

1.2. Scope of the Study

1.3. Definition

Chapter 2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.3. Assumptions & Limitations

Chapter 3. Executive Summary

3.1. Market Snapshot

Chapter 4. Market Variables and Scope

4.1. Introduction

4.2. Market Classification and Scope

4.3. Industry Value Chain Analysis

4.3.1. Raw Material Procurement Analysis

4.3.2. Sales and Distribution Channel Analysis

4.3.3. Downstream Buyer Analysis

Chapter 5. COVID 19 Impact on Vessel Sealing Devices Market

5.1. COVID-19 Landscape: Vessel Sealing Devices Industry Impact

5.2. COVID 19 - Impact Assessment for the Industry

5.3. COVID 19 Impact: Global Major Government Policy

5.4. Market Trends and Opportunities in the COVID-19 Landscape

Chapter 6. Market Dynamics Analysis and Trends

6.1. Market Dynamics

6.1.1. Market Drivers

6.1.2. Market Restraints

6.1.3. Market Opportunities

6.2. Porter’s Five Forces Analysis

6.2.1. Bargaining power of suppliers

6.2.2. Bargaining power of buyers

6.2.3. Threat of substitute

6.2.4. Threat of new entrants

6.2.5. Degree of competition

Chapter 7. Competitive Landscape

7.1.1. Company Market Share/Positioning Analysis

7.1.2. Key Strategies Adopted by Players

7.1.3. Vendor Landscape

7.1.3.1. List of Suppliers

7.1.3.2. List of Buyers

Chapter 8. Global Vessel Sealing Devices Market, By Application

8.1. Vessel Sealing Devices Market, by Application, 2023-2032

8.1.1 General Surgery

8.1.1.1. Market Revenue and Forecast (2019-2032)

8.1.2. Laparoscopic Surgery

8.1.2.1. Market Revenue and Forecast (2019-2032)

Chapter 9. Global Vessel Sealing Devices Market, By Product

9.1. Vessel Sealing Devices Market, by Product, 2023-2032

9.1.1. Generators

9.1.1.1. Market Revenue and Forecast (2019-2032)

9.1.2. Instruments

9.1.2.1. Market Revenue and Forecast (2019-2032)

9.1.3. Accessories

9.1.3.1. Market Revenue and Forecast (2019-2032)

Chapter 10. Global Vessel Sealing Devices Market, By End-use

10.1. Vessel Sealing Devices Market, by End-use, 2023-2032

10.1.1. Hospitals & Specialty Clinics

10.1.1.1. Market Revenue and Forecast (2019-2032)

10.1.2. Ambulatory Surgical Centers

10.1.2.1. Market Revenue and Forecast (2019-2032)

Chapter 11. Global Vessel Sealing Devices Market, Regional Estimates and Trend Forecast

11.1. North America

11.1.1. Market Revenue and Forecast, by Application (2019-2032)

11.1.2. Market Revenue and Forecast, by Product (2019-2032)

11.1.3. Market Revenue and Forecast, by End-use (2019-2032)

11.1.4. U.S.

11.1.4.1. Market Revenue and Forecast, by Application (2019-2032)

11.1.4.2. Market Revenue and Forecast, by Product (2019-2032)

11.1.4.3. Market Revenue and Forecast, by End-use (2019-2032)

11.1.5. Rest of North America

11.1.5.1. Market Revenue and Forecast, by Application (2019-2032)

11.1.5.2. Market Revenue and Forecast, by Product (2019-2032)

11.1.5.3. Market Revenue and Forecast, by End-use (2019-2032)

11.2. Europe

11.2.1. Market Revenue and Forecast, by Application (2019-2032)

11.2.2. Market Revenue and Forecast, by Product (2019-2032)

11.2.3. Market Revenue and Forecast, by End-use (2019-2032)

11.2.4. UK

11.2.4.1. Market Revenue and Forecast, by Application (2019-2032)

11.2.4.2. Market Revenue and Forecast, by Product (2019-2032)

11.2.4.3. Market Revenue and Forecast, by End-use (2019-2032)

11.2.5. Germany

11.2.5.1. Market Revenue and Forecast, by Application (2019-2032)

11.2.5.2. Market Revenue and Forecast, by Product (2019-2032)

11.2.5.3. Market Revenue and Forecast, by End-use (2019-2032)

11.2.6. France

11.2.6.1. Market Revenue and Forecast, by Application (2019-2032)

11.2.6.2. Market Revenue and Forecast, by Product (2019-2032)

11.2.6.3. Market Revenue and Forecast, by End-use (2019-2032)

11.2.7. Rest of Europe

11.2.7.1. Market Revenue and Forecast, by Application (2019-2032)

11.2.7.2. Market Revenue and Forecast, by Product (2019-2032)

11.2.7.3. Market Revenue and Forecast, by End-use (2019-2032)

11.3. APAC

11.3.1. Market Revenue and Forecast, by Application (2019-2032)

11.3.2. Market Revenue and Forecast, by Product (2019-2032)

11.3.3. Market Revenue and Forecast, by End-use (2019-2032)

11.3.4. India

11.3.4.1. Market Revenue and Forecast, by Application (2019-2032)

11.3.4.2. Market Revenue and Forecast, by Product (2019-2032)

11.3.4.3. Market Revenue and Forecast, by End-use (2019-2032)

11.3.5. China

11.3.5.1. Market Revenue and Forecast, by Application (2019-2032)

11.3.5.2. Market Revenue and Forecast, by Product (2019-2032)

11.3.5.3. Market Revenue and Forecast, by End-use (2019-2032)

11.3.6. Japan

11.3.6.1. Market Revenue and Forecast, by Application (2019-2032)

11.3.6.2. Market Revenue and Forecast, by Product (2019-2032)

11.3.6.3. Market Revenue and Forecast, by End-use (2019-2032)

11.3.7. Rest of APAC

11.3.7.1. Market Revenue and Forecast, by Application (2019-2032)

11.3.7.2. Market Revenue and Forecast, by Product (2019-2032)

11.3.7.3. Market Revenue and Forecast, by End-use (2019-2032)

11.4. MEA

11.4.1. Market Revenue and Forecast, by Application (2019-2032)

11.4.2. Market Revenue and Forecast, by Product (2019-2032)

11.4.3. Market Revenue and Forecast, by End-use (2019-2032)

11.4.4. GCC

11.4.4.1. Market Revenue and Forecast, by Application (2019-2032)

11.4.4.2. Market Revenue and Forecast, by Product (2019-2032)

11.4.4.3. Market Revenue and Forecast, by End-use (2019-2032)

11.4.5. North Africa

11.4.5.1. Market Revenue and Forecast, by Application (2019-2032)

11.4.5.2. Market Revenue and Forecast, by Product (2019-2032)

11.4.5.3. Market Revenue and Forecast, by End-use (2019-2032)

11.4.6. South Africa

11.4.6.1. Market Revenue and Forecast, by Application (2019-2032)

11.4.6.2. Market Revenue and Forecast, by Product (2019-2032)

11.4.6.3. Market Revenue and Forecast, by End-use (2019-2032)

11.4.7. Rest of MEA

11.4.7.1. Market Revenue and Forecast, by Application (2019-2032)

11.4.7.2. Market Revenue and Forecast, by Product (2019-2032)

11.4.7.3. Market Revenue and Forecast, by End-use (2019-2032)

11.5. Latin America

11.5.1. Market Revenue and Forecast, by Application (2019-2032)

11.5.2. Market Revenue and Forecast, by Product (2019-2032)

11.5.3. Market Revenue and Forecast, by End-use (2019-2032)

11.5.4. Brazil

11.5.4.1. Market Revenue and Forecast, by Application (2019-2032)

11.5.4.2. Market Revenue and Forecast, by Product (2019-2032)

11.5.4.3. Market Revenue and Forecast, by End-use (2019-2032)

11.5.5. Rest of LATAM

11.5.5.1. Market Revenue and Forecast, by Application (2019-2032)

11.5.5.2. Market Revenue and Forecast, by Product (2019-2032)

11.5.5.3. Market Revenue and Forecast, by End-use (2019-2032)

Chapter 12. Company Profiles

12.1. Medtronic

12.1.1. Company Overview

12.1.2. Product Offerings

12.1.3. Financial Performance

12.1.4. Recent Initiatives

12.2. Olympus Corporation

12.2.1. Company Overview

12.2.2. Product Offerings

12.2.3. Financial Performance

12.2.4. Recent Initiatives

12.3. B. Braun Melsungen AG

12.3.1. Company Overview

12.3.2. Product Offerings

12.3.3. Financial Performance

12.3.4. Recent Initiatives

12.4. Medical Devices Business Services, Inc. (Johnson & Johnson)

12.4.1. Company Overview

12.4.2. Product Offerings

12.4.3. Financial Performance

12.4.4. Recent Initiatives

12.5. Erbe Elektromedizin GmbH

12.5.1. Company Overview

12.5.2. Product Offerings

12.5.3. Financial Performance

12.5.4. Recent Initiatives

12.6. Bowa Medical

12.6.1. Company Overview

12.6.2. Product Offerings

12.6.3. Financial Performance

12.6.4. Recent Initiatives

12.7. OmniGuide Holdings, Inc.

12.7.1. Company Overview

12.7.2. Product Offerings

12.7.3. Financial Performance

12.7.4. Recent Initiatives

12.8. Intuitive Surgical

12.8.1. Company Overview

12.8.2. Product Offerings

12.8.3. Financial Performance

12.8.4. Recent Initiatives

12.9. Bolder Surgical LLC

12.9.1. Company Overview

12.9.2. Product Offerings

12.9.3. Financial Performance

12.9.4. Recent Initiatives

12.10. KLS Martin Group

12.10.1. Company Overview

12.10.2. Product Offerings

12.10.3. Financial Performance

12.10.4. Recent Initiatives

Chapter 13. Research Methodology

13.1. Primary Research

13.2. Secondary Research

13.3. Assumptions

Chapter 14. Appendix

14.1. About Us

14.2. Glossary of Terms

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers