Flexible Endoscopes Market Size, Share | Report 2023-2032

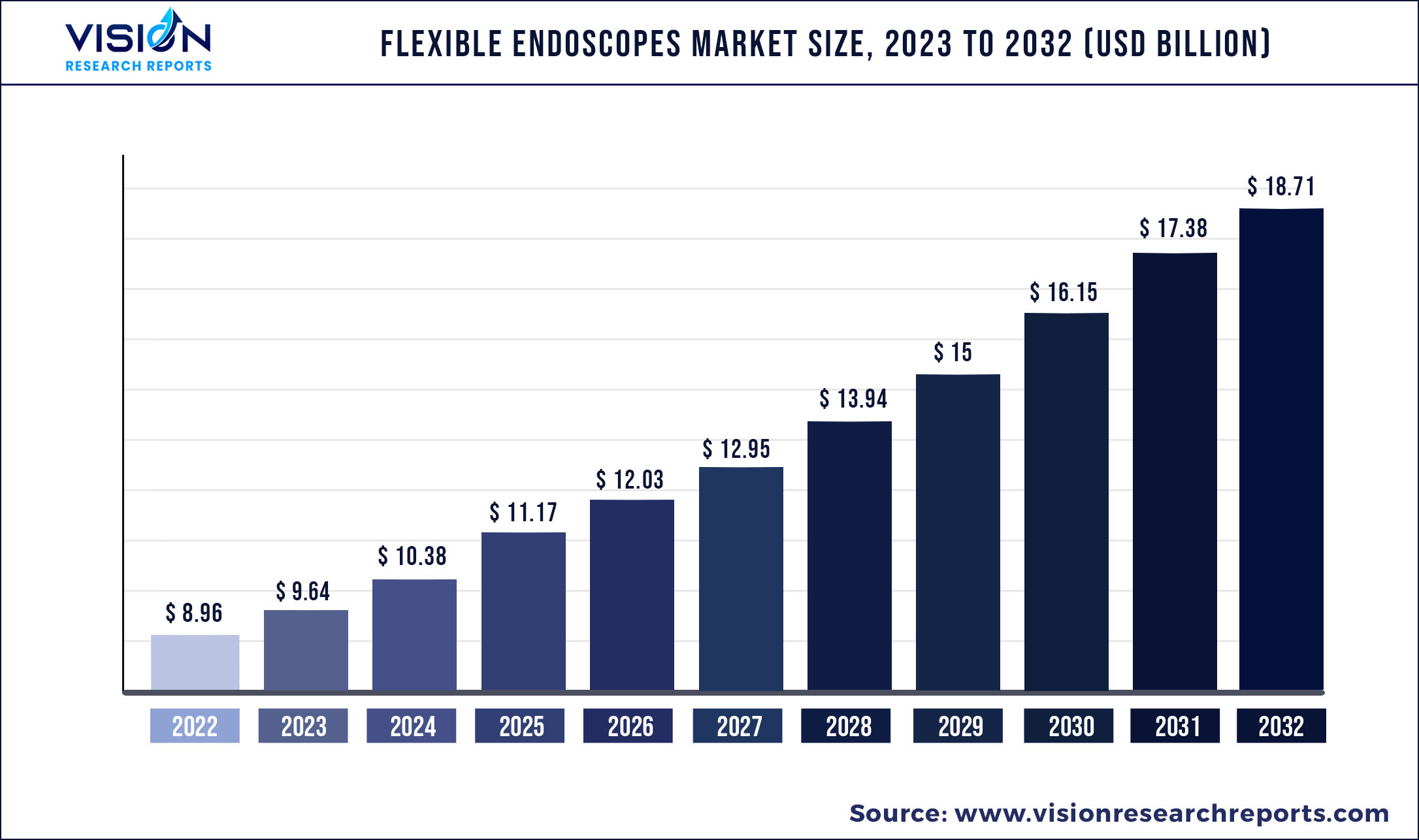

The global flexible endoscopes market was valued at USD 8.96 billion in 2022 and it is predicted to surpass around USD 18.71 billion by 2032 with a CAGR of 7.64% from 2023 to 2032.

Key Pointers

Report Scope of the Flexible Endoscopes Market

| Report Coverage | Details |

| Market Size in 2022 | USD 8.96 billion |

| Revenue Forecast by 2032 | USD 18.71 billion |

| Growth rate from 2023 to 2032 | CAGR of 7.64% |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Market Analysis (Terms Used) | Value (US$ Million/Billion) or (Volume/Units) |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Companies Covered | Olympus Corporation; Ethicon Endo-surgery; LLC.; FUJIFILM Holdings Corporation; Stryker Corporation; Boston Scientific Corporation; Karl Storz GmbH & Co. KG.; Smith & Nephew Inc.; Richard Wolf GmbH; Medtronic Plc (Covidien); Ambu A/S; PENTAX Medical and Machida Endoscope Co., Ltd. |

The increasing use of minimally invasive surgical procedures has led to a growing demand for various types of endoscopes and endoscopy devices in surgical interventions, such as cystoscopy, bronchoscopy, arthroscopy, and laparoscopy. This shift towards minimally invasive surgeries over traditional surgeries is attributable to multiple reasons such as cost-effectiveness, higher patient satisfaction, shorter hospital stays, and fewer post-surgical complications.

The COVID-19 pandemic disrupted various industries worldwide including the medical sector, which experienced significant impacts such as disruptions in treatment procedures and healthcare services, as well as challenges with the supply chain of medical devices. The market was also affected, with a decrease in demand for new endoscopes due to a reduction in endoscopy services being offered in hospitals due to COVID-19-related emergencies on healthcare staff. In February 2021, according to an article published by the Guidelines for Robotic Flexible Endoscopy at the Time of COVID-19, endoscopic procedures were significantly reduced during the pandemic, and only urgent cases were considered.

The COVID-19 pandemic affected the demand for these endoscopes due to certain endoscopic procedures, such as respiratory endoscopy and gastrointestinal endoscopy, being considered aerosol-generating procedures for SARS-CoV-2 transmission. For instance, the American Association for Bronchology & Interventional Pulmonology updated its recommendations for using flexible bronchoscopes in COVID-19 patients. The updated recommendations indicated that bronchoscopy posed a substantial risk to patients and staff as an aerosol-generating procedure. As a result, bronchoscopy was not the preferred option for diagnosing COVID-19 and was only considered for intubated patients if upper respiratory samples were negative. These factors contributed to a decrease in demand for flexible endoscopes and impacted the studied market during the COVID-19 pandemic.

Furthermore, factors driving the market include an increase in the prevalence of chronic diseases affecting internal body systems, the advantages of flexible endoscopes compared to other devices, and growing awareness for early diagnosis of these conditions. Inflammatory bowel diseases (IBD), stomach & colon cancers, respiratory infections, and tumors, among others, require the use of these devices for diagnosis. As a result, the growth in the incidence of these diseases has led to an increase in demand for these flexible devices. For instance, in 2022, the American Cancer Society, Inc. estimated that there were about 26,380 new cases of stomach cancer (15,900 in men and 10,480 in women) in the U.S., as well as 106,180 new cases of colon cancer and 44,850 new cases of rectal cancer.

The high incidence and prevalence of chronic diseases such as lung cancer and irritable bowel syndrome in the U.S. are driving the demand for the use of flexible endoscopes. For example, the American Lung Association estimated that 236,000 people in the U.S. were diagnosed with lung cancer in 2021, while the American College of Gastroenterology reports that 10-15% of adults suffer from irritable bowel syndrome symptoms in the country. Moreover, the advantages of flexible endoscopes over other types are also contributing to their increasing use, with optical fiber being particularly advantageous due to its ability to change direction and expand its scope of application.

Flexible Endoscopes Market Segmentations:

By Type

By End-use

Chapter 1. Introduction

1.1. Research Objective

1.2. Scope of the Study

1.3. Definition

Chapter 2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.3. Assumptions & Limitations

Chapter 3. Executive Summary

3.1. Market Snapshot

Chapter 4. Market Variables and Scope

4.1. Introduction

4.2. Market Classification and Scope

4.3. Industry Value Chain Analysis

4.3.1. Raw Material Procurement Analysis

4.3.2. Sales and Distribution Channel Analysis

4.3.3. Downstream Buyer Analysis

Chapter 5. COVID 19 Impact on Flexible Endoscopes Market

5.1. COVID-19 Landscape: Flexible Endoscopes Industry Impact

5.2. COVID 19 - Impact Assessment for the Industry

5.3. COVID 19 Impact: Global Major Government Policy

5.4. Market Trends and Opportunities in the COVID-19 Landscape

Chapter 6. Market Dynamics Analysis and Trends

6.1. Market Dynamics

6.1.1. Market Drivers

6.1.2. Market Restraints

6.1.3. Market Opportunities

6.2. Porter’s Five Forces Analysis

6.2.1. Bargaining power of suppliers

6.2.2. Bargaining power of buyers

6.2.3. Threat of substitute

6.2.4. Threat of new entrants

6.2.5. Degree of competition

Chapter 7. Competitive Landscape

7.1.1. Company Market Share/Positioning Analysis

7.1.2. Key Strategies Adopted by Players

7.1.3. Vendor Landscape

7.1.3.1. List of Suppliers

7.1.3.2. List of Buyers

Chapter 8. Global Flexible Endoscopes Market, By Type

8.1. Flexible Endoscopes Market, by Type, 2023-2032

8.1.1. Laparoscopes

8.1.1.1. Market Revenue and Forecast (2020-2032)

8.1.2. Arthroscopes

8.1.2.1. Market Revenue and Forecast (2020-2032)

8.1.3. Ureteroscopes

8.1.3.1. Market Revenue and Forecast (2020-2032)

8.1.4. Cystoscopes

8.1.4.1. Market Revenue and Forecast (2020-2032)

8.1.5. Gynecology Endoscopes

8.1.5.1. Market Revenue and Forecast (2020-2032)

8.1.6. Neuroendoscopes

8.1.6.1. Market Revenue and Forecast (2020-2032)

8.1.7. Bronchoscopes

8.1.7.1. Market Revenue and Forecast (2020-2032)

8.1.8. Hysteroscopes

8.1.8.1. Market Revenue and Forecast (2020-2032)

8.1.9. Laryngoscopes

8.1.9.1. Market Revenue and Forecast (2020-2032)

8.1.10. Sinuscopes

8.1.10.1. Market Revenue and Forecast (2020-2032)

8.1.11. Otoscopes

8.1.11.1. Market Revenue and Forecast (2020-2032)

8.1.12. Sigmoidoscopes

8.1.12.1. Market Revenue and Forecast (2020-2032)

8.1.13. Pharyngoscopes

8.1.13.1. Market Revenue and Forecast (2020-2032)

8.1.14. Duodenoscope

8.1.14.1. Market Revenue and Forecast (2020-2032)

8.1.15. Nasopharyngoscopes

8.1.15.1. Market Revenue and Forecast (2020-2032)

8.1.16. Rhinoscopes

8.1.16.1. Market Revenue and Forecast (2020-2032)

8.1.17. Colonoscopes

8.1.17.1. Market Revenue and Forecast (2020-2032)

Chapter 9. Global Flexible Endoscopes Market, By End-use

9.1. Flexible Endoscopes Market, by End-use, 2023-2032

9.1.1. Hospitals

9.1.1.1. Market Revenue and Forecast (2020-2032)

9.1.2. Outpatient Facilities

9.1.2.1. Market Revenue and Forecast (2020-2032)

Chapter 10. Global Flexible Endoscopes Market, Regional Estimates and Trend Forecast

10.1. North America

10.1.1. Market Revenue and Forecast, by Type (2020-2032)

10.1.2. Market Revenue and Forecast, by End-use (2020-2032)

10.1.3. U.S.

10.1.3.1. Market Revenue and Forecast, by Type (2020-2032)

10.1.3.2. Market Revenue and Forecast, by End-use (2020-2032)

10.1.4. Rest of North America

10.1.4.1. Market Revenue and Forecast, by Type (2020-2032)

10.1.4.2. Market Revenue and Forecast, by End-use (2020-2032)

10.2. Europe

10.2.1. Market Revenue and Forecast, by Type (2020-2032)

10.2.2. Market Revenue and Forecast, by End-use (2020-2032)

10.2.3. UK

10.2.3.1. Market Revenue and Forecast, by Type (2020-2032)

10.2.3.2. Market Revenue and Forecast, by End-use (2020-2032)

10.2.4. Germany

10.2.4.1. Market Revenue and Forecast, by Type (2020-2032)

10.2.4.2. Market Revenue and Forecast, by End-use (2020-2032)

10.2.5. France

10.2.5.1. Market Revenue and Forecast, by Type (2020-2032)

10.2.5.2. Market Revenue and Forecast, by End-use (2020-2032)

10.2.6. Rest of Europe

10.2.6.1. Market Revenue and Forecast, by Type (2020-2032)

10.2.6.2. Market Revenue and Forecast, by End-use (2020-2032)

10.3. APAC

10.3.1. Market Revenue and Forecast, by Type (2020-2032)

10.3.2. Market Revenue and Forecast, by End-use (2020-2032)

10.3.3. India

10.3.3.1. Market Revenue and Forecast, by Type (2020-2032)

10.3.3.2. Market Revenue and Forecast, by End-use (2020-2032)

10.3.4. China

10.3.4.1. Market Revenue and Forecast, by Type (2020-2032)

10.3.4.2. Market Revenue and Forecast, by End-use (2020-2032)

10.3.5. Japan

10.3.5.1. Market Revenue and Forecast, by Type (2020-2032)

10.3.5.2. Market Revenue and Forecast, by End-use (2020-2032)

10.3.6. Rest of APAC

10.3.6.1. Market Revenue and Forecast, by Type (2020-2032)

10.3.6.2. Market Revenue and Forecast, by End-use (2020-2032)

10.4. MEA

10.4.1. Market Revenue and Forecast, by Type (2020-2032)

10.4.2. Market Revenue and Forecast, by End-use (2020-2032)

10.4.3. GCC

10.4.3.1. Market Revenue and Forecast, by Type (2020-2032)

10.4.3.2. Market Revenue and Forecast, by End-use (2020-2032)

10.4.4. North Africa

10.4.4.1. Market Revenue and Forecast, by Type (2020-2032)

10.4.4.2. Market Revenue and Forecast, by End-use (2020-2032)

10.4.5. South Africa

10.4.5.1. Market Revenue and Forecast, by Type (2020-2032)

10.4.5.2. Market Revenue and Forecast, by End-use (2020-2032)

10.4.6. Rest of MEA

10.4.6.1. Market Revenue and Forecast, by Type (2020-2032)

10.4.6.2. Market Revenue and Forecast, by End-use (2020-2032)

10.5. Latin America

10.5.1. Market Revenue and Forecast, by Type (2020-2032)

10.5.2. Market Revenue and Forecast, by End-use (2020-2032)

10.5.3. Brazil

10.5.3.1. Market Revenue and Forecast, by Type (2020-2032)

10.5.3.2. Market Revenue and Forecast, by End-use (2020-2032)

10.5.4. Rest of LATAM

10.5.4.1. Market Revenue and Forecast, by Type (2020-2032)

10.5.4.2. Market Revenue and Forecast, by End-use (2020-2032)

Chapter 11. Company Profiles

11.1. Olympus Corporation

11.1.1. Company Overview

11.1.2. Product Offerings

11.1.3. Financial Performance

11.1.4. Recent Initiatives

11.2. Ethicon Endo-surgery; LLC.

11.2.1. Company Overview

11.2.2. Product Offerings

11.2.3. Financial Performance

11.2.4. Recent Initiatives

11.3. FUJIFILM Holdings Corporation

11.3.1. Company Overview

11.3.2. Product Offerings

11.3.3. Financial Performance

11.3.4. Recent Initiatives

11.4. Stryker Corporation

11.4.1. Company Overview

11.4.2. Product Offerings

11.4.3. Financial Performance

11.4.4. LTE Scientific

11.5. Boston Scientific Corporation

11.5.1. Company Overview

11.5.2. Product Offerings

11.5.3. Financial Performance

11.5.4. Recent Initiatives

11.6. Karl Storz GmbH & Co. KG.

11.6.1. Company Overview

11.6.2. Product Offerings

11.6.3. Financial Performance

11.6.4. Recent Initiatives

11.7. Smith & Nephew Inc.

11.7.1. Company Overview

11.7.2. Product Offerings

11.7.3. Financial Performance

11.7.4. Recent Initiatives

11.8. Richard Wolf GmbH

11.8.1. Company Overview

11.8.2. Product Offerings

11.8.3. Financial Performance

11.8.4. Recent Initiatives

11.9. Medtronic Plc (Covidien)

11.9.1. Company Overview

11.9.2. Product Offerings

11.9.3. Financial Performance

11.9.4. Recent Initiatives

11.10. Ambu A/S

11.10.1. Company Overview

11.10.2. Product Offerings

11.10.3. Financial Performance

11.10.4. Recent Initiatives

Chapter 12. Research Methodology

12.1. Primary Research

12.2. Secondary Research

12.3. Assumptions

Chapter 13. Appendix

13.1. About Us

13.2. Glossary of Terms

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers