Ultrasound Device Market Size, Share | Report 2023-2032

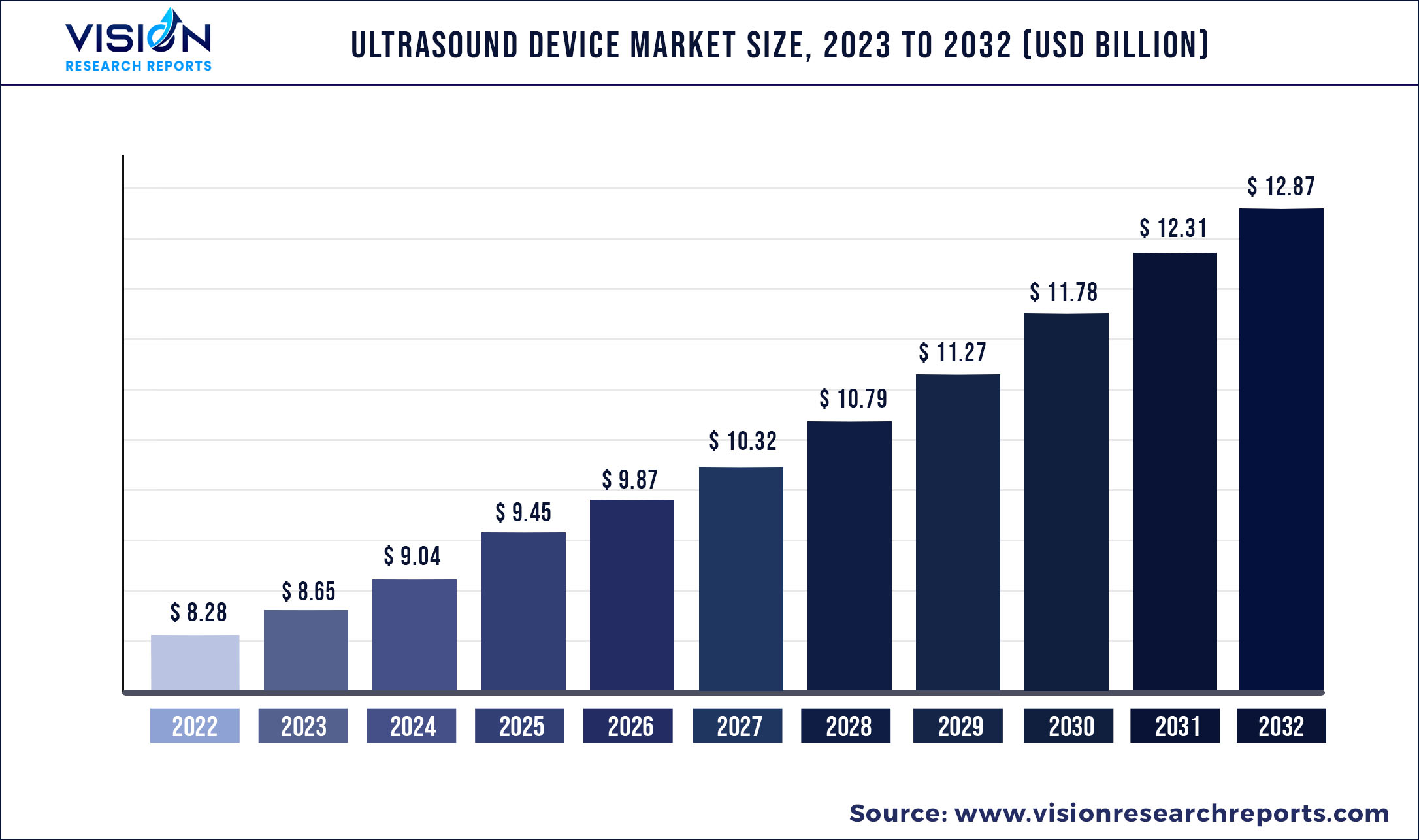

The global ultrasound device market was estimated at USD 8.28 billion in 2022 and it is expected to surpass around USD 12.87 billion by 2032, poised to grow at a CAGR of 4.51% from 2023 to 2032.

Key Pointers

Report Scope of the Ultrasound Device Market

| Report Coverage | Details |

| Market Size in 2022 | USD 8.28 billion |

| Revenue Forecast by 2032 | USD 12.87 billion |

| Growth rate from 2023 to 2032 | CAGR of 4.51% |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Market Analysis (Terms Used) | Value (US$ Million/Billion) or (Volume/Units) |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

The rise in the adoption of ultrasound devices for diagnostic imaging and treatment, coupled with the increasing incidences of chronic and lifestyle-related disorders, is expected to boost the market growth. In addition, the rising demand for minimally invasive surgery and technological advancements in ultrasound imaging technology are some of the key factors driving the market. Ultrasound is considered one of the most valuable diagnostic tools in medical imaging due to the fact that it is fast and less expensive. In addition, it is safer than other imaging technologies as it does not utilize ionizing radiation and magnetic field.

The ultrasonic medical device has a wide range of diagnostic as well as therapeutic applications. Ultrasonography has become more popular for specific therapeutic applications, ranging from cardiology to oncology. The expansion of ultrasound device applications in 3D imaging, shear wave elastography, development of wireless transducers, app-based ultrasound technology, fusion with CT/MR, and laparoscopic ultrasound is set to keep the market excited for the near future. For instance, Samsung Medison collaborated with Intel for NerveTrack, a real-time nerve tracking ultrasonography technology that helps anesthesiologists detect nerves in a patient's arm and deliver anesthesia swiftly and precisely.

Furthermore, the integration of artificial intelligence (Al) to automate time-consuming processes such as quantification and selecting the best image slice from a 3-D dataset is expected to boost the market growth. Many high-end ultrasound systems now use AI, and most new systems at all levels are expected to include AI in the future. The healthcare system had faced enormous difficulties as a result of the COVID-19 pandemic. The demand for ultrasound devices was uneven during the pandemic as there were postponements in installations and a drop in manufacturing was also observed. Manufacturers had to focus on COVID essential device manufacturing and COVID tackling methods such as telehealth services, vaccination drives for employees, and others. However, the handheld ultrasound device was in high demand owing to its efficiency in treating critical care patients in crowded hospitals because of the systems’ speed, portability, and ease of use.

Key Companies & Market Share Insights

The major players are working to improve their product offerings by upgrading their products, taking advantage of important cooperation activities, and exploring acquisitions and government clearances in order to expand their customer base and gain a larger share of the overall market. For instance, in March 2021, GE Healthcare introduced Vscan Air, a wireless pocket-sized ultrasound that gives crystal clear image quality, whole-body scanning capability, and intuitive software, all in the palm of clinicians’ hands. Some of the prominent players in the global ultrasound device market include:

Ultrasound Device Market Segmentations:

By Product

By Portability

By Application

By End-use

Chapter 1. Introduction

1.1. Research Objective

1.2. Scope of the Study

1.3. Definition

Chapter 2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.3. Assumptions & Limitations

Chapter 3. Executive Summary

3.1. Market Snapshot

Chapter 4. Market Variables and Scope

4.1. Introduction

4.2. Market Classification and Scope

4.3. Industry Value Chain Analysis

4.3.1. Raw Material Procurement Analysis

4.3.2. Sales and Distribution Channel Analysis

4.3.3. Downstream Buyer Analysis

Chapter 5. COVID 19 Impact on Ultrasound Device Market

5.1. COVID-19 Landscape: Ultrasound Device Industry Impact

5.2. COVID 19 - Impact Assessment for the Industry

5.3. COVID 19 Impact: Global Major Government Policy

5.4. Market Trends and Opportunities in the COVID-19 Landscape

Chapter 6. Market Dynamics Analysis and Trends

6.1. Market Dynamics

6.1.1. Market Drivers

6.1.2. Market Restraints

6.1.3. Market Opportunities

6.2. Porter’s Five Forces Analysis

6.2.1. Bargaining power of suppliers

6.2.2. Bargaining power of buyers

6.2.3. Threat of substitute

6.2.4. Threat of new entrants

6.2.5. Degree of competition

Chapter 7. Competitive Landscape

7.1.1. Company Market Share/Positioning Analysis

7.1.2. Key Strategies Adopted by Players

7.1.3. Vendor Landscape

7.1.3.1. List of Suppliers

7.1.3.2. List of Buyers

Chapter 8. Global Ultrasound Device Market, By Product

8.1. Ultrasound Device Market, by Product, 2023-2032

8.1.1. Diagnostic Ultrasound Devices

8.1.1.1. Market Revenue and Forecast (2020-2032)

8.1.2. Therapeutic Ultrasound Devices

8.1.2.1. Market Revenue and Forecast (2020-2032)

Chapter 9. Global Ultrasound Device Market, By Portability

9.1. Ultrasound Device Market, by Portability, 2023-2032

9.1.1. Handheld

9.1.1.1. Market Revenue and Forecast (2020-2032)

9.1.2. Cart/Trolley

9.1.2.1. Market Revenue and Forecast (2020-2032)

Chapter 10. Global Ultrasound Device Market, By Application

10.1. Ultrasound Device Market, by Application, 2023-2032

10.1.1. Cardiology

10.1.1.1. Market Revenue and Forecast (2020-2032)

10.1.2. Obstetrics/Gynaecology

10.1.2.1. Market Revenue and Forecast (2020-2032)

10.1.3. Vascular

10.1.3.1. Market Revenue and Forecast (2020-2032)

10.1.4. Orthopedic

10.1.4.1. Market Revenue and Forecast (2020-2032)

10.1.5. General Imaging

10.1.5.1. Market Revenue and Forecast (2020-2032)

Chapter 11. Global Ultrasound Device Market, By End-use

11.1. Ultrasound Device Market, by End-use, 2023-2032

11.1.1. Hospitals

11.1.1.1. Market Revenue and Forecast (2020-2032)

11.1.2. Imaging Centres

11.1.2.1. Market Revenue and Forecast (2020-2032)

11.1.3. Research Centres

11.1.3.1. Market Revenue and Forecast (2020-2032)

Chapter 12. Global Ultrasound Device Market, Regional Estimates and Trend Forecast

12.1. North America

12.1.1. Market Revenue and Forecast, by Product (2020-2032)

12.1.2. Market Revenue and Forecast, by Portability (2020-2032)

12.1.3. Market Revenue and Forecast, by Application (2020-2032)

12.1.4. Market Revenue and Forecast, by End-use (2020-2032)

12.1.5. U.S.

12.1.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.1.5.2. Market Revenue and Forecast, by Portability (2020-2032)

12.1.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.1.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.1.6. Rest of North America

12.1.6.1. Market Revenue and Forecast, by Product (2020-2032)

12.1.6.2. Market Revenue and Forecast, by Portability (2020-2032)

12.1.6.3. Market Revenue and Forecast, by Application (2020-2032)

12.1.6.4. Market Revenue and Forecast, by End-use (2020-2032)

12.2. Europe

12.2.1. Market Revenue and Forecast, by Product (2020-2032)

12.2.2. Market Revenue and Forecast, by Portability (2020-2032)

12.2.3. Market Revenue and Forecast, by Application (2020-2032)

12.2.4. Market Revenue and Forecast, by End-use (2020-2032)

12.2.5. UK

12.2.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.2.5.2. Market Revenue and Forecast, by Portability (2020-2032)

12.2.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.2.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.2.6. Germany

12.2.6.1. Market Revenue and Forecast, by Product (2020-2032)

12.2.6.2. Market Revenue and Forecast, by Portability (2020-2032)

12.2.6.3. Market Revenue and Forecast, by Application (2020-2032)

12.2.6.4. Market Revenue and Forecast, by End-use (2020-2032)

12.2.7. France

12.2.7.1. Market Revenue and Forecast, by Product (2020-2032)

12.2.7.2. Market Revenue and Forecast, by Portability (2020-2032)

12.2.7.3. Market Revenue and Forecast, by Application (2020-2032)

12.2.7.4. Market Revenue and Forecast, by End-use (2020-2032)

12.2.8. Rest of Europe

12.2.8.1. Market Revenue and Forecast, by Product (2020-2032)

12.2.8.2. Market Revenue and Forecast, by Portability (2020-2032)

12.2.8.3. Market Revenue and Forecast, by Application (2020-2032)

12.2.8.4. Market Revenue and Forecast, by End-use (2020-2032)

12.3. APAC

12.3.1. Market Revenue and Forecast, by Product (2020-2032)

12.3.2. Market Revenue and Forecast, by Portability (2020-2032)

12.3.3. Market Revenue and Forecast, by Application (2020-2032)

12.3.4. Market Revenue and Forecast, by End-use (2020-2032)

12.3.5. India

12.3.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.3.5.2. Market Revenue and Forecast, by Portability (2020-2032)

12.3.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.3.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.3.6. China

12.3.6.1. Market Revenue and Forecast, by Product (2020-2032)

12.3.6.2. Market Revenue and Forecast, by Portability (2020-2032)

12.3.6.3. Market Revenue and Forecast, by Application (2020-2032)

12.3.6.4. Market Revenue and Forecast, by End-use (2020-2032)

12.3.7. Japan

12.3.7.1. Market Revenue and Forecast, by Product (2020-2032)

12.3.7.2. Market Revenue and Forecast, by Portability (2020-2032)

12.3.7.3. Market Revenue and Forecast, by Application (2020-2032)

12.3.7.4. Market Revenue and Forecast, by End-use (2020-2032)

12.3.8. Rest of APAC

12.3.8.1. Market Revenue and Forecast, by Product (2020-2032)

12.3.8.2. Market Revenue and Forecast, by Portability (2020-2032)

12.3.8.3. Market Revenue and Forecast, by Application (2020-2032)

12.3.8.4. Market Revenue and Forecast, by End-use (2020-2032)

12.4. MEA

12.4.1. Market Revenue and Forecast, by Product (2020-2032)

12.4.2. Market Revenue and Forecast, by Portability (2020-2032)

12.4.3. Market Revenue and Forecast, by Application (2020-2032)

12.4.4. Market Revenue and Forecast, by End-use (2020-2032)

12.4.5. GCC

12.4.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.4.5.2. Market Revenue and Forecast, by Portability (2020-2032)

12.4.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.4.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.4.6. North Africa

12.4.6.1. Market Revenue and Forecast, by Product (2020-2032)

12.4.6.2. Market Revenue and Forecast, by Portability (2020-2032)

12.4.6.3. Market Revenue and Forecast, by Application (2020-2032)

12.4.6.4. Market Revenue and Forecast, by End-use (2020-2032)

12.4.7. South Africa

12.4.7.1. Market Revenue and Forecast, by Product (2020-2032)

12.4.7.2. Market Revenue and Forecast, by Portability (2020-2032)

12.4.7.3. Market Revenue and Forecast, by Application (2020-2032)

12.4.7.4. Market Revenue and Forecast, by End-use (2020-2032)

12.4.8. Rest of MEA

12.4.8.1. Market Revenue and Forecast, by Product (2020-2032)

12.4.8.2. Market Revenue and Forecast, by Portability (2020-2032)

12.4.8.3. Market Revenue and Forecast, by Application (2020-2032)

12.4.8.4. Market Revenue and Forecast, by End-use (2020-2032)

12.5. Latin America

12.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.5.2. Market Revenue and Forecast, by Portability (2020-2032)

12.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.5.5. Brazil

12.5.5.1. Market Revenue and Forecast, by Product (2020-2032)

12.5.5.2. Market Revenue and Forecast, by Portability (2020-2032)

12.5.5.3. Market Revenue and Forecast, by Application (2020-2032)

12.5.5.4. Market Revenue and Forecast, by End-use (2020-2032)

12.5.6. Rest of LATAM

12.5.6.1. Market Revenue and Forecast, by Product (2020-2032)

12.5.6.2. Market Revenue and Forecast, by Portability (2020-2032)

12.5.6.3. Market Revenue and Forecast, by Application (2020-2032)

12.5.6.4. Market Revenue and Forecast, by End-use (2020-2032)

Chapter 13. Company Profiles

13.1. Koninklijke Philips N.V.

13.1.1. Company Overview

13.1.2. Product Offerings

13.1.3. Financial Performance

13.1.4. Recent Initiatives

13.2. GE Healthcare

13.2.1. Company Overview

13.2.2. Product Offerings

13.2.3. Financial Performance

13.2.4. Recent Initiatives

13.3. Siemens Healthineers AG

13.3.1. Company Overview

13.3.2. Product Offerings

13.3.3. Financial Performance

13.3.4. Recent Initiatives

13.4. Canon Medical Systems

13.4.1. Company Overview

13.4.2. Product Offerings

13.4.3. Financial Performance

13.4.4. Recent Initiatives

13.5. Mindray Medical International Limited

13.5.1. Company Overview

13.5.2. Product Offerings

13.5.3. Financial Performance

13.5.4. Recent Initiatives

13.6. Samsung Medison Co., Ltd.

13.6.1. Company Overview

13.6.2. Product Offerings

13.6.3. Financial Performance

13.6.4. Recent Initiatives

13.7. FUJIFILM SonoSite, Inc.

13.7.1. Company Overview

13.7.2. Product Offerings

13.7.3. Financial Performance

13.7.4. Recent Initiatives

13.8. Konica Minolta Inc.

13.8.1. Company Overview

13.8.2. Product Offerings

13.8.3. Financial Performance

13.8.4. Recent Initiatives

13.9. Esaote

13.9.1. Company Overview

13.9.2. Product Offerings

13.9.3. Financial Performance

13.9.4. Recent Initiatives

Chapter 14. Research Methodology

14.1. Primary Research

14.2. Secondary Research

14.3. Assumptions

Chapter 15. Appendix

15.1. About Us

15.2. Glossary of Terms

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers